Legal Update

Feb 27, 2013

Issue 53: Final Rules Issued on Essential Health Benefits, Actuarial and Minimum Valuation

This is the fifty-third issue in our health care reform series of alerts for employers on selected topics in health care reform. (Our general summary of health care reform and other issues in this series can be accessed by clicking here). This series of Health Care Reform Management Alerts is designed to provide a more in-depth analysis of certain aspects of health care reform and how it will impact your employer-sponsored plans.

The Department of Health and Human Services (HSS) issued final rules published in the February 25th Federal Register related to essential health benefits (EHB) that must be covered beginning in 2014 by individual and small group health insurance issuers under the Affordable Care Act (ACA). HHS also issued a fact sheet on the rule.

While HHS noted it had received approximately 11,000 comments related to EHB, the final rules state that HHS already considered these comments as it drafted the proposed rule. As a result, the final rule largely adopted the approach in the proposed regulations discussed in Issue 46.

The final rule does include a few changes and clarifications, including the following:

-

Limit on Deductibles for Non-Grandfathered Health Plans Only for Small Group Market. As discussed in more detail in Issue 52, the preamble to the final rules provides that the limit on deductibles for non-grandfathered he

-

Nondiscrimination Rules. The final rule adopts the proposed regulations’ provision that prohibits an issuer from discriminating in benefit design and implementation based on an individual’s age, expected length of life, present or predicted disability, degree of medical dependency, quality of life or other health condition. The final rule clarifies, however, that an issuer may still appropriately utilize reasonable medical management techniques.

-

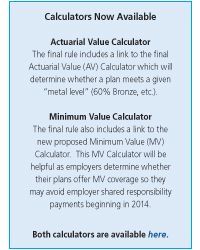

HSA and Integrated HRA Contributions. The final rule clarifies that employer contributions to HSAs and new employer contributions to integrated HRAs that are offered in connection with a medical plan (as opposed to stand alone HRAs) may be taken into account for purposes of the Actuarial Value (AV) Calculation and Minimum Value (MV) Calculation.

-

Habilitative Services. As noted in Issue 46, self-funded plans cannot apply annual or lifetime limits to “essential health benefits”, as defined in the benchmark plan chosen by the self-funded plan. Among the list of required essential health benefits are habilitative and rehabilitative services. Because many health insurance plans do not identify habilitative services as a distinct group of services, the final rule adopts the proposed regulations’ approach to include a transitional policy for coverage of habilitative services that would provide states with the opportunity to define these benefits if they were not included in the base-benchmark plan. Specifically, if the base-benchmark plan did not include coverage of habilitative services, the state would be permitted to determine the services included in the habilitative services category. If states did not define the habilitative services category, plans would be required to provide benefits that are similar in scope, amount and duration to benefits covered for rehabilitative services, or that are determined by the insurance issuer and reported to HHS. HHS indicated it intends to carefully monitor coverage of habilitative services across the individual and small group markets, and to use this data to inform future changes to this transitional policy.

Seyfarth Shaw LLP provides this information as a service to clients and other friends for educational purposes only. It should not be construed or relied on as legal advice or to create a lawyer-client relationship. Readers should not act upon this information without seeking advice from their professional advisers.