We launched Seyfarth’s Future Employer initiative in 2017, as the Fourth Industrial Revolution transformed the workplace. Since then, nearly every aspect of work has changed. We have tracked these changes through a multi-year survey of employers grappling with these issues. Our 2022 follow-up survey shows that employers are largely optimistic and resilient, with faith in their people, their organizations, and their own future-readiness. However, many of our respondents are not yet embracing future technology, such as the metaverse and cryptocurrency. The highlights from our survey provide a frame into current thinking of today’s business leaders.

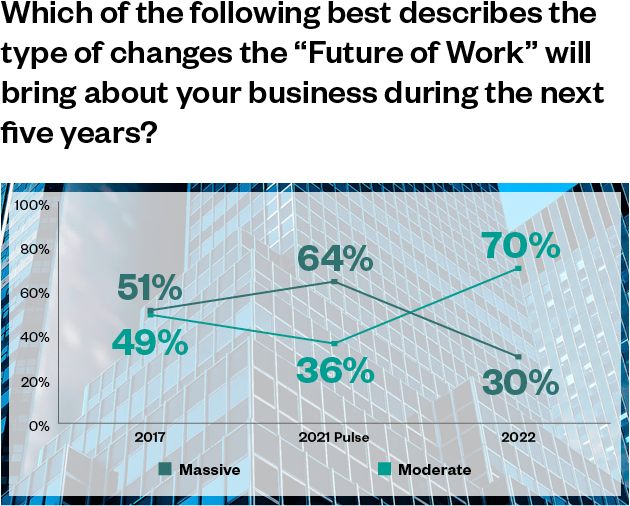

Massive Change Behind?

In 2017, respondents were nearly evenly split on whether change would be massive or moderate in nature. The pandemic shifted the tide toward more massive change, as indicated in our 2021 pulse survey. However, since the pandemic, more and more respondents foresee moderate change on the horizon. With the mass closures of COVID-19 behind us, the expectation of more moderate change indicates that many employers think we have now weathered a period of extreme upheaval—and are perhaps still acclimating to the massive changes of the last two years.

Tempered Optimism

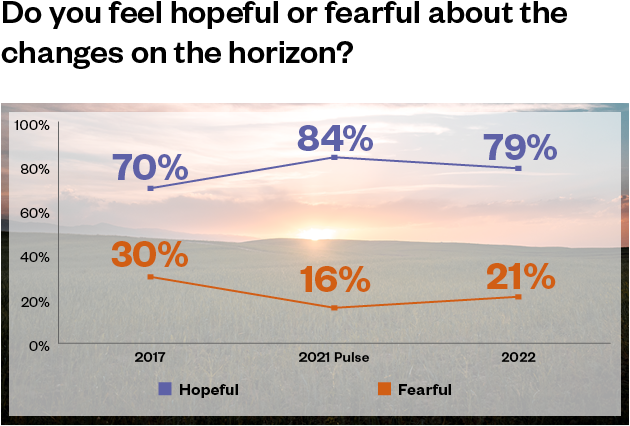

In 2021, we saw a slight bump in the overall optimism of our respondents, perhaps fueled by the easing of COVID restrictions. While still overwhelmingly optimistic, the number of those feeling fearful in our recent survey went up, with respondents citing social isolation, loss of engagement, the "culture wars," and potential recession as reasons for their answers.

A conversation about drivers of fear in 2022 would be missing the critical mention of Russia’s invasion of Ukraine. The sanctions (and counter-sanctions) that followed with lightning speed, caught many multinationals unprepared. Companies were faced with a true Hobson’s choice: Continue profitable operations in Russia and face the Western world’s scorn (while driving returns to shareholders and continuing to employ people in Russia), or support the sanctions and walk away, often at substantial short-term cost and with potentially criminal risk to local managers. Given the uncertainty, both choices stunk.

The world is staring straight into a once-in-a-lifetime shift—a Zeitenwende—in world politics. Nations face a geopolitical landscape where relations between nations are often more transactional, opportunistic, and short-lived. But many multinational corporations come into this new “pop-up alliance” era unequipped, their structures and strategies forged during the relative predictability of the Cold War and the post-Cold War eras. But globalization means that geopolitical conflict can disrupt supply chains that affect the entire global economy. Sophisticated multinationals must develop a new kind of corporate strategy to survive and succeed. The most successful global companies must view strategy as an integrated whole of: Traditional corporate strategy, a flexible but strong human capital philosophy, and a comprehensive corporate geopolitical approach that underlies it all.

Considering all three together—strategy, people, and geopolitics—provides the greatest hedge against the unknowns of this new era.

Meeting in the Middle

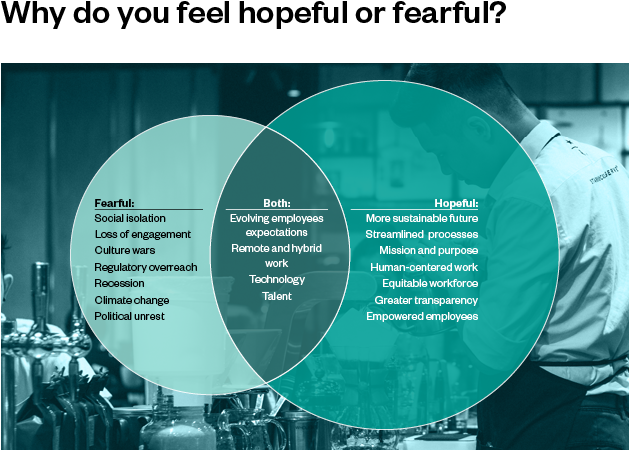

When asked why they were hopeful or fearful, respondents cited everything from social isolation and the "culture wars" (fearful), to a more sustainable future and human-centered work (hopeful). Interestingly, several topics were cited as reasons for being fearful and for being hopeful, including evolving employee expectations, remote and hybrid work, technology, and talent. The results show that employers see both the challenges and opportunities in these top-of-mind topics.

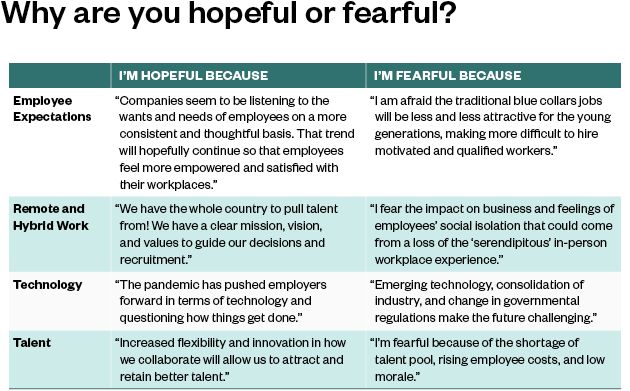

See below for verbatim responses from "both sides" of the hopeful or fearful divide on the shared topics.

Hopeful quotes:

- “Companies seem to be listening to the wants and needs of employees on a more consistent and thoughtful basis. That trend will hopefully continue so that employees feel more empowered and satisfied with their workplaces.”

- “We have the whole country to pull talent from! We have a clear mission, vision, and values to guide our decisions and recruitment.”

- “The pandemic has pushed employers forward in terms of technology and questioning how things get done.”

- “Increased flexibility and innovation in how we collaborate will allow us to attract and retain better talent.”

Fearful quotes:

- “I fear the impact on business and feelings of employees’ social isolation that could come from a loss of the 'serendipitous' in-person workplace experience.”

- “I am afraid the traditional blue collar jobs will be less and less attractive for the young generations, making it more difficult to hire motivated and qualified workers.”

- “Emerging technology, consolidation of industry, and change in governmental regulations make the future challenging.”

- “I’m fearful because of the shortage of talent pool, rising employee costs, and low morale.”

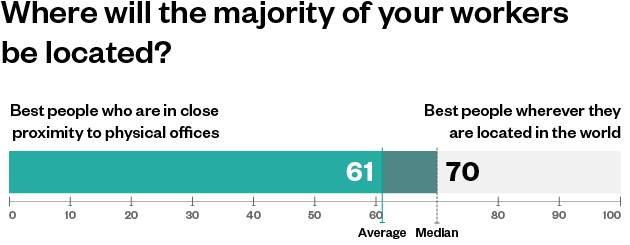

Proximity Power

While hybrid workforces and flexibility are here to stay, our respondents tell us that proximity still has power. When asked where their employees would be located, respondents on average said that 61% of their workforces would be located near a physical office, with a median response of 70%.

On the surface the data suggest that most respondents see a future with workers close to the physical office. There currently is no easy or risk-free way to hire people wherever they are in the world. Employing people “anywhere” requires consideration of employment, tax, and immigration, among other issues. Given this complexity and associated cost, few employers are actually doing it, although many are crafting related policies and processes that make sense for their organizations. As a result, what the survey data shows may be premature. Further, those who are hiring "anywhere" tend to be in certain industries structurally suited to this type of work arrangement, and who look to hire hard-to-fill roles.

Digital Dangers

With the dramatic increase in the number of remote workers over the last three years, many companies pushed the limits of their existing technology infrastructures. Our survey shows that many have considered the potential information security, privacy, and compliance ramifications of remote access, and will continue to remain vigilant against threats by increasing their security postures.

Even before COVID, employers have worked hard shoring up their proprietary data. With employers allowing employees to work from anywhere—even if just temporarily—existing risk points take on far greater significance.

For instance, the increase in international travel enhances the likelihood that a foreign government will access workers’ computers and devices when they pass through immigration. Few people understand that immigration officials have the right to insist that travelers comply with a request to log in to their devices. Should officials wish to image the person’s device, they could do so with virtual impunity. Similarly, while traveling in foreign jurisdictions that have the capability to monitor internet traffic, it similarly exposes companies’ intellectual property—in many cases with no recourse.

Similarly, if a remote worker saves company information on their personal computer, outside of litigation, the company will struggle (and perhaps fail) to get that information back from the employee's personal device in many locations in the world. Employers need to have a thoughtful, well-implemented strategy for effectively "sandboxing" any personal device that touches employer data. This includes policies, technical, and administrative controls associated with the misappropriation and misuse of proprietary information.

Forward-thinking employers are considering these issues together, as they’re all inextricably linked, and working to develop holistic policies that allow companies to attract and retain the talent they need, where they need it, without risking their “crown jewels”—talent and intellectual property—in the process.

Tech Transparency

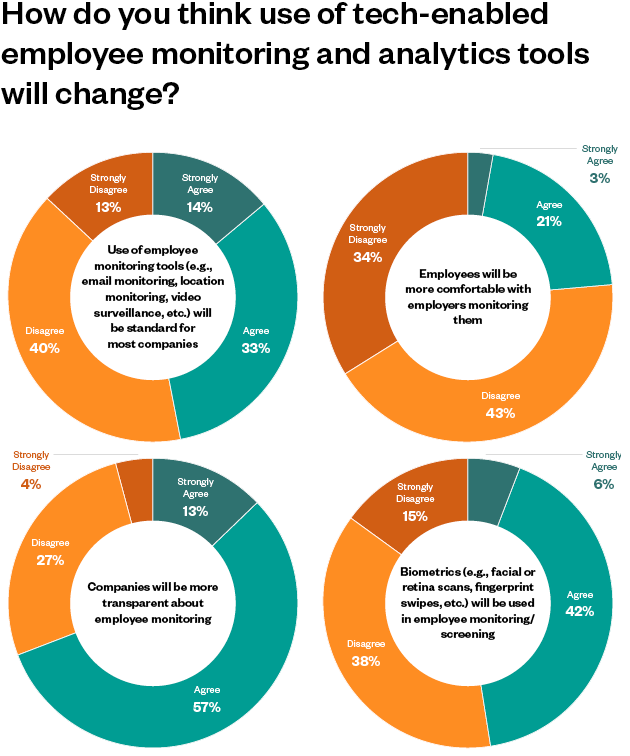

While our respondents agreed that use of tech-enabled employee monitoring and analytics tools would go up, they also said overwhelmingly that employees would not be comfortable with this change. Ultimately, employers will be more transparent about monitoring because it’s the smart thing to do, and because regulations will require it. While employees may accept monitoring, they will perhaps never be comfortable with it, even with increased transparency. Employers must weigh the desire to monitor and the advantages gained against the implicit message they are sending to their employees. From a purely regulatory point of view, not all clients are aware of their privacy obligations, which can potentially get them into legal trouble along with the potential of damage to employee relations and related psychosocial risks.

Numbers are rounded so percentages may not add up to 100%.

Alternative Rules

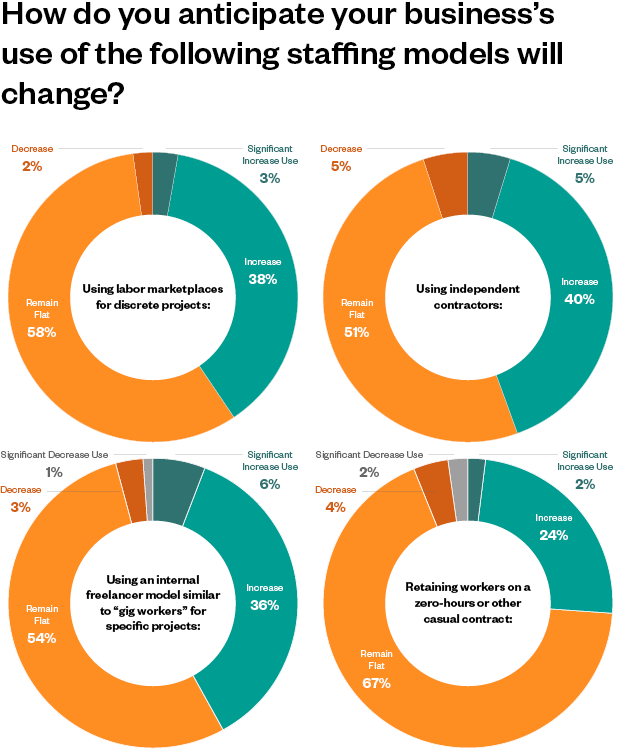

When it comes to alternative staffing, our respondents showed a preference for the “traditional” use of independent contractors, rather than other models such as labor marketplaces, internal gig work, and zero-hour or casual contracts. This could be because businesses have not yet seen how newer alternative models can work in practice. They may also be alarmed by the regulation growing up around the use of “gig economy” workers, especially in Europe, or the assumed cost of such models. Ultimately, the use of alternative staffing will come down to what type of resource the business can use, what the competition for talent is like, what type of contract that talent will accept, and the employer’s overall risk tolerance.

Numbers are rounded so percentages may not add up to 100%.

Although using contractors is a common approach, it is important for employers to understand that it still has the potential to be high risk. Contractor arrangements can morph into employment. This can be costly down the line, especially where local tax authorities and other authorities become involved. So for clients who have the use of contractors in mind, we recommend putting in place strict guardrails on how they use contractors and, importantly, keeping these arrangements under regular review. Global principles can be put in place, even though the local risks and specifics vary.

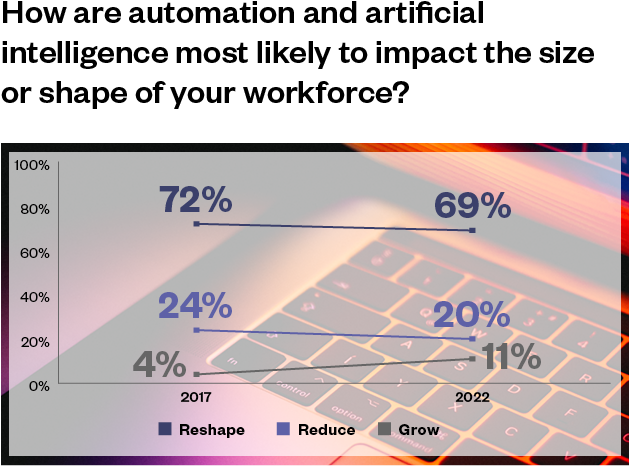

Tech-Enabled Growth?

In the last five years, we have seen an uptick in respondents expecting the use of artificial intelligence to increase the size of their workforces. Accordingly, those who said they expect their workforces to be reduced because of artificial intelligence shrank.

This trend goes against conventional wisdom about automation and AI replacing workers and is perhaps an indication that our respondents have accelerated tech-enabled initiatives within their companies. New technologies have always created more jobs than they’ve destroyed in the past, and as workplaces take advantage of artificial intelligence, humans will have an opportunity to leverage the innate traits that machines cannot offer: creativity, expertise, and relationships.

Not Banking on Crypto

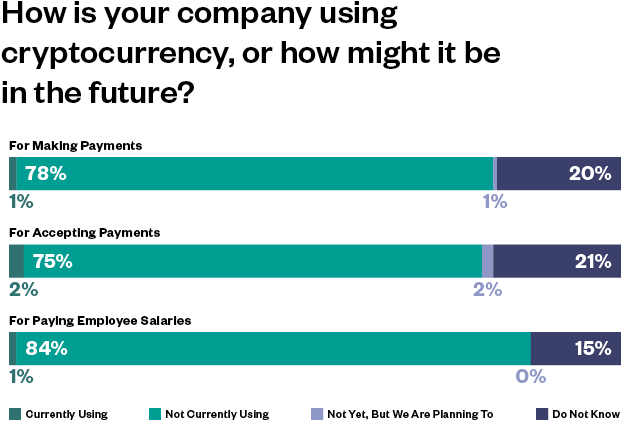

The vast majority of our respondents are not using cryptocurrency for making payments, accepting payments, or paying employee salaries. For many companies, crypto is simply far too volatile. Furthermore, the technology infrastructure required to use cryptocurrency makes it far too impractical for many businesses, and the architecture of the current crypto platforms aren't at the level to scale for mass consumer transactions.

If the advantages of crypto grow to outweigh the challenges, many businesses will see it as a way to appeal to new demographics and to keep up with suppliers and business partners who are moving to crypto.

Metaverse or Meta-worse?

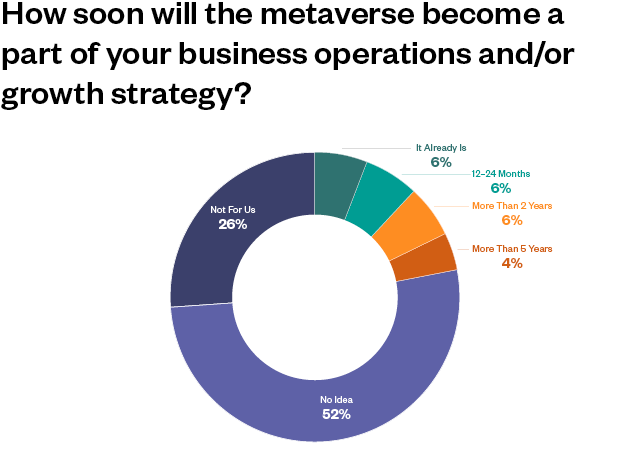

The concept of the metaverse is very much at an early stage and early adopters who are investing in and using the metaverse are still working out how it benefits them. Many more companies have either written off the metaverse as a fad or have not even considered whether the metaverse is relevant to them or their customers. Accordingly, nearly 78% of our respondents indicated that the metaverse isn't for their organizations, or they have no idea how it will be incorporated into their operations or strategy into the future.

For many who have invested in the metaverse to date, it has primarily been as part of a marketing strategy. If we see the number of dominant metaverses increase, clients may need to move quickly to harness whatever markets they present. We expect the numbers of those who answer affirmatively to grow over time as the competitive advantages become more widely understood. Those advantages include AI driven services, ownership of digital property, and innovation through virtual reality experiences.

In the current economic climate and post- crypto and NFT crashes, healthy cynicism around the metaverse prevails. Even so, companies shouldn’t write it off. There are already quasi-metaverses (such as massively multiplayer online games) that have enormous numbers of users. It will take some time, but ultimately the metaverse will find its place—we just don’t know what that is yet, and odds are it’ll be focused initially on gaming.

Meet the Team

Our attorneys are here to help you understand the changing landscape of the workplace, to shape, guide, and suggest new approaches to work, and to navigate the continuing evolution of the laws that will serve as the framework of our future.

If you have any questions about the survey or your business needs, please get in touch with our Future of Work expert panel: futureofworkexperts@seyfarth.com.

Related practice areas:

Methodology

Seyfarth surveyed in-house legal and business leaders via online survey for a one-month period between August and September 2022. A total of 200 respondents completed the survey. Respondents included General Counsel, Directors of HR, Associate General Counsel, HR Managers, Presidents, Senior Counsel, VP, HR and a number of other titles from industries including consumer discretionary, consumer staples, energy, financial services, health care, industrials, information technology, materials, real estate, telecommunication services, and utilities. Verbatim responses were edited for length and clarity.